Nature fintech series: Putting natural capital on the map

By: Raviv Turner, Founding Member of the Nature Tech Collective

Digital financial technology (otherwise known as fintech) is well-known in today’s landscape for having revolutionized global financial systems by improving customer experiences, speeding up banking processes, and simplifying investment decisions. Although historically, the banking sector has not extended itself to reconsider its relationship with the state of nature in the pursuit of capital growth.

As our understanding of new economic models has grown to account for natural resource extraction, carbon emissions, and waste management cycles, opportunities to rethink the link between nature and the economy have arisen. But individual financial actors have not necessarily followed suit.

In today’s economy, nearly 7 trillion USD of financial flows still go towards nature-negative industries such as construction, electric utilities, real estate, oil and gas, food, agriculture, and tobacco industries according to a recent report published by the UN Environment Programme (UNEP). This is more than ten times greater than public finance flows to Nature-Based Solutions (NbS), estimated at USD 200 billion annually.

As an emerging space, the boundless innovative possibilities of fintech present a unique opportunity to mobilize more capital in pursuit of a nature-positive economy. This is where the niche of nature fintech comes in. Nature fintech combines financial services and products with digital technologies to drive investments towards nature conservation, restoration, and sustainable use of natural resources. It aims to create economic incentives and viable business models that benefit the environment and address critical issues like deforestation, biodiversity loss, water management, and sustainable agriculture.

Over the next few weeks, the Nature Tech Collective (NTC) will launch its inaugural Nature Fintech Series to unravel this new digital ecosystem of natural capital catalysts. NTC’s Fintech Series will explore these crucial intersections through a number of articles and a detailed mapping of the nature fintech market. This will all culminate in an in-depth report and a working group to further explore these intersections and opportunities.

Our research explores three key questions:

How should we define nature fintech and what are the overlaps and contrasts between nature vs. climate fintech?

Where do areas of natural capital opportunity exist – what business models and digital technologies are successful in practice?

How do nature fintech companies grow – what financial stakeholders and innovation frameworks must engage for these companies to have maximum impact?

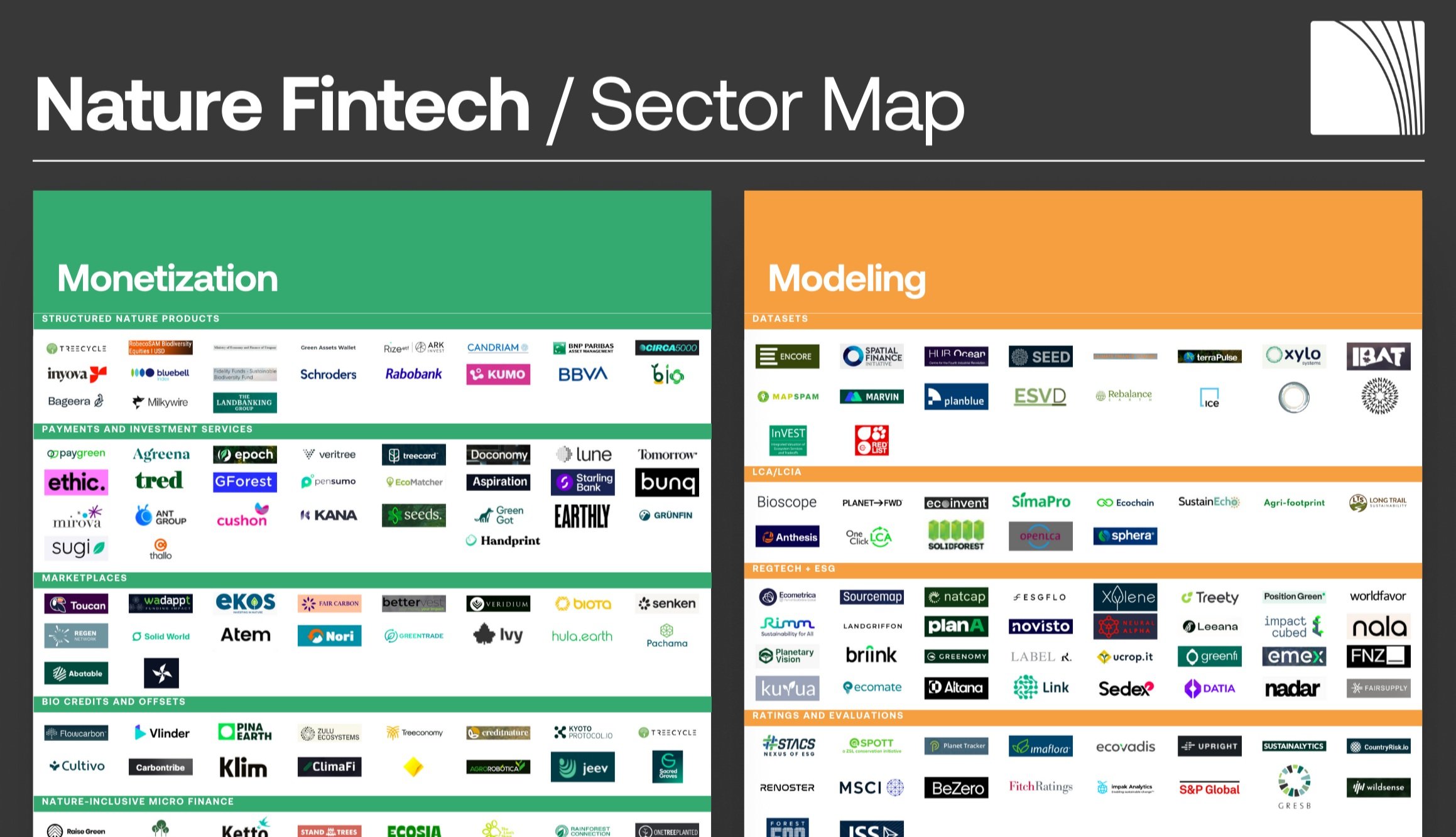

The sector map and future report will serve as a distillation of over 200 interviews from 2023 with financial institutions, banking experts, ecosystem and biodiversity scientists, nature VCs, and nature fintech startups, among others. This is the first of what we hope to be many endeavors to better understand where areas of opportunities exist, and how to best bring them to scale. Initial findings have yielded a growing database of more than 200 “nature fintech” companies from around the world that can be accessed with Nature Tech Collective membership.

The 4 Ms

We see businesses and initiatives in the sector shaping into four categories, what we call the four M’s.

-

What are the entities and frameworks that drive actors to solve for nature-related market failures, providing tools and frameworks to reach these goals? One example of this is the wave of mandatory and voluntary reporting frameworks such as the TNFD, CSRD, SBTN, EUDR, California SB253 & SB 261. Other sector actors include NGOs, industry associations, framework providers, and international cooperation institutions. Their main role(s) are identifying and closing gaps in capital mobilization that expose market actors to risk and assisting businesses in mitigating/eliminating overshoot of planetary bounds.

-

This category is essential to assess the state of nature and natural assets for use cases across the financial sector. Biodiversity assessments (in situ and ex situ) allow companies to measure and quantify their positive and negative impacts on nature. This data enables them to disclose impact and dependencies, risk and opportunities, and report against compliance frameworks such as the TNFD, CSRD, SBTN, EUDR, California SB253 & SB 261 and to monitor impacts on nature over time.

-

Raw nature data is not very useful for corporations on its own. The modeling category includes organizations that clean, index, analyze, visualize, and model nature data for the benefit of corporations and other entities. On their own, this is too big of a task for any organization interested in viewing their financial impact on nature.

Nature data modeling services benefit the insurance and regulation sectors along with resource-related technologies that provide clients with faster, more efficient, and more transparent understandings of their operations and dependencies, making it possible to financially quantify nature risks and opportunities.

The tools used most at this level are big data solutions: AI, machine learning, and large language models that have proven to navigate the complexity of company value chain dependencies. Organizations in this category use the primary data generated from organizations in the following measurement category to create tools from input-output tables to client-tailored solutions.

-

Monetization encompasses organizations that use technology for facilitating, securing, or recording natural capital transactions. Solutions that provide alternative financial market instruments for nature are considered part of the monetization category such as green bonds, credits and offsets, and ETFs. Tech-enabled marketplaces for credits and offsets are also included here and show a large degree of overlap with climate solutions. This category contains standalone products used for crowdsourcing, investing, and payments that enable corporations and individuals alike to induce nature-positive financial flows.

Additional Details

In the sector map and future report, we also explore how applied digital technologies such as big data, artificial intelligence (AI), and blockchain, can overcome incumbent challenges of natural capital, in areas like limited access to capital, opaque nature accounting, and the cost-burden of nature debt issuance.

Lastly, we analyze how big-picture frameworks such as crowdfunding, platform marketplaces, biodiversity credit schemes, and open banking can create additional incentives and accessibility for nature-conscious stakeholder participation.

This is our first exercise to kickstart and map the process as an exploratory phase. We would like to extend an invitation to all parties interested in collaborating for further exploration of this sector.

Please note that the report and sector map do not intend to be-all and end-all for the developing and dynamic space of nature fintech. This is our first industry-wide attempt to map the space, point at gaps, and provide a strategic positioning tool for all players in the space. We intend to update this report periodically and keep a dynamic database of companies. You can submit your comments, feedback, and/or your nature-positive company using this form.

------

I would also like to extend a special thank you to the Nature Tech Collective research team, led by Paula Palermo and Owen Dehmler- Buckley for their diligent work in the last few months in working to publish the report and sector map.

To view the sector map, click here.